| 🚩 Keywords: LightGBM, LSTM, GRU, ERCOT, Energy Markets, SHAP, Rolling-Origin CV | GitHub |

This project was completed by Jessalyn Chuang, Neha Manish Shah, Michelle Schultze, and Zixiao Tan (Prairie Dog Team) for the Spring 2025 section of IDS 705: Principles of Machine Learning at Duke University.

Overview

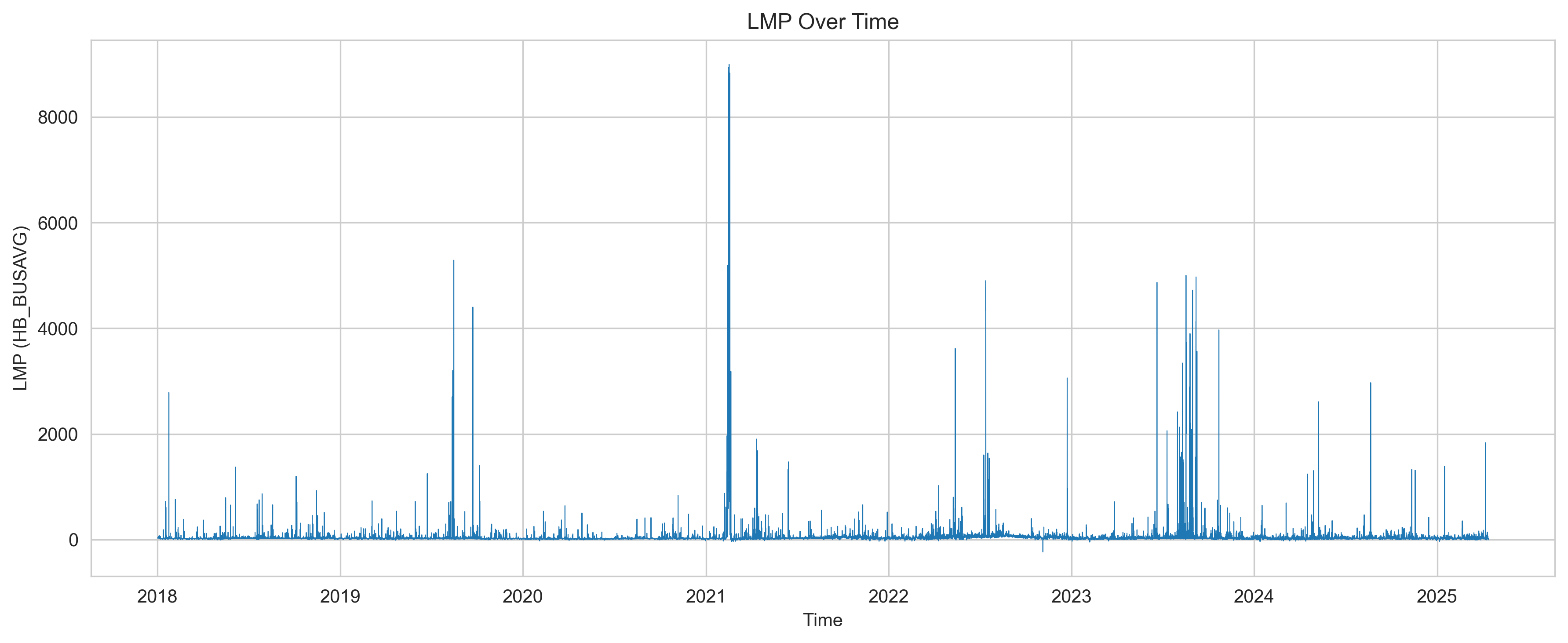

Electricity prices in wholesale energy markets are notoriously volatile, driven by demand spikes, renewable intermittency, and fuel cost fluctuations. Accurate short-term price forecasting enables grid operators, traders, and policymakers to make better decisions. This project benchmarks tree-based and deep learning models for forecasting ERCOT (Electric Reliability Council of Texas) hub prices across multiple time horizons using only publicly available data.

Target Variable

ERCOT Average Hub Real-Time Locational Marginal Price (LMP) — the wholesale electricity price ($/MWh) at the system hub, sampled hourly.

Data Sources

| Source | Features |

|---|---|

| GridStatus.io | Real-time ERCOT load, generation fuel mix (wind, solar, gas, coal), solar generation |

| EIA (Energy Information Administration) | Regional electricity demand and supply statistics |

| Plano, TX Weather Station | Hourly dry-bulb and wet-bulb temperatures |

| Henry Hub Natural Gas | Daily spot prices |

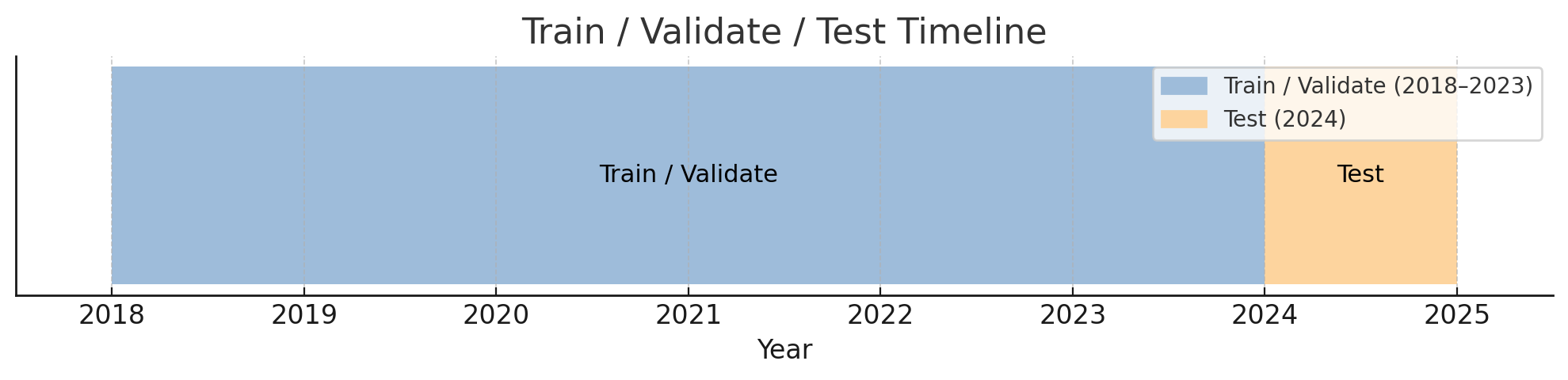

- Time period: 2018 – 2025

- Granularity: Hourly (aligned via forward-fill for daily series)

- Processed dataset: ~60,000 hourly observations after cleaning

Feature Engineering

- Lagged LMP values (1h, 24h, 168h)

- Hour-of-day, day-of-week, month cyclical encodings

- Rolling means and standard deviations of load and generation

- Wet-bulb temperature (heat stress proxy)

- Natural gas price as fuel cost signal

Models

| Model | Type | Best For |

|---|---|---|

| LightGBM | Gradient Boosted Trees | 1-hour ahead forecasting |

| XGBoost | Gradient Boosted Trees | Baseline comparison |

| LSTM | Recurrent Neural Network | 1-day ahead forecasting |

| GRU | Recurrent Neural Network | 1-day ahead forecasting |

Hyperparameters tuned using Optuna (Bayesian optimization). All models evaluated on rolling-origin cross-validation — a time-aware resampling strategy that prevents data leakage.

Results Summary

| Horizon | Best Model | Key Metric |

|---|---|---|

| 1-hour ahead | LightGBM | Lowest MAE & RMSE |

| 1-day ahead | LSTM / GRU | Outperform tree methods |

| 1-week ahead | Mixed | High uncertainty across all models |

Observation: Tree-based models capture short-term autocorrelation efficiently; recurrent networks better model the multi-step temporal dependencies at the 1-day horizon.

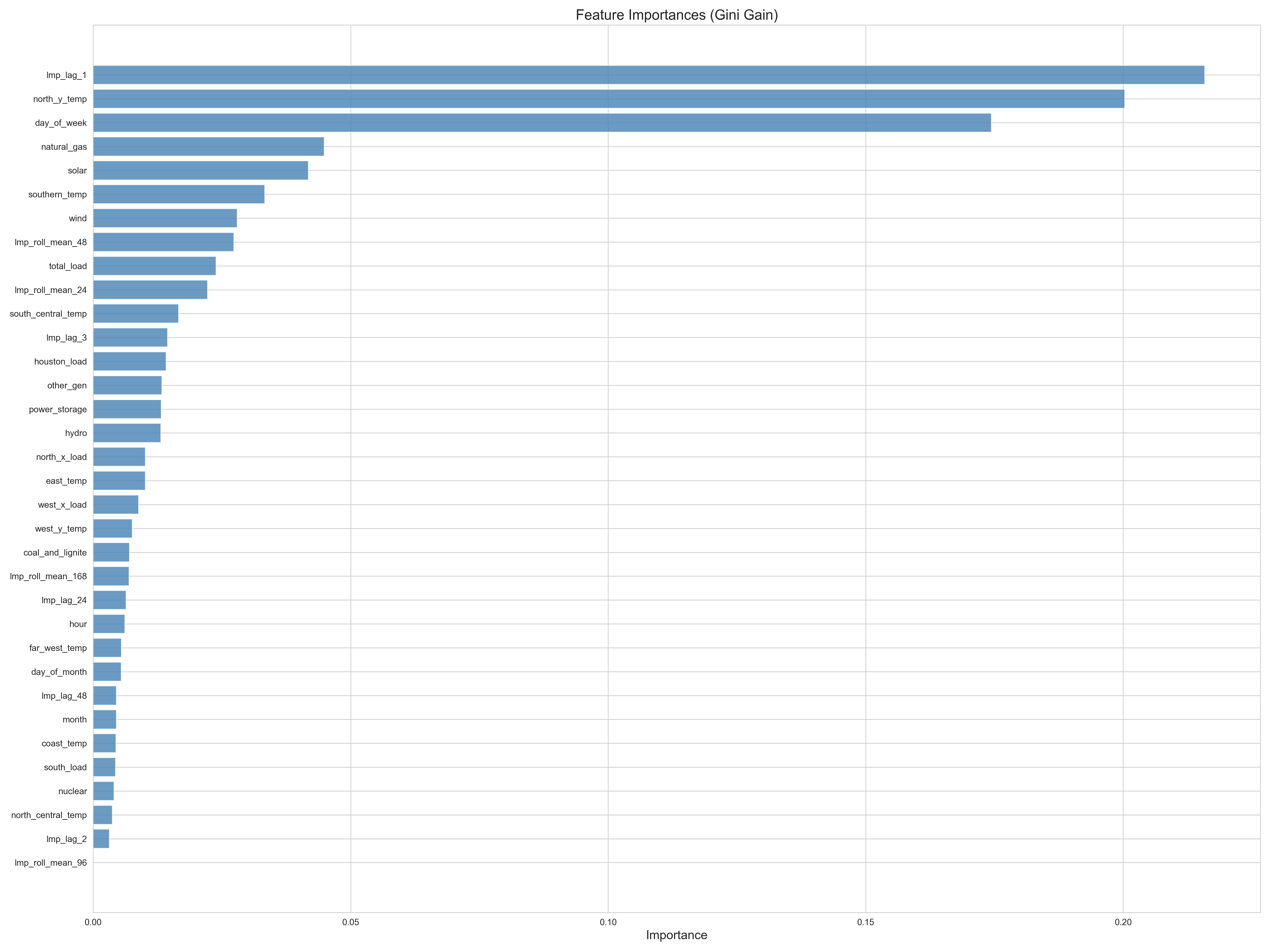

Feature Importance (SHAP Analysis)

The most predictive features across all models:

- Lagged LMP prices (1h and 24h lags) — strongest signal

- Regional temperatures — demand-side proxy

- Natural gas price — supply-side cost driver

- Time-of-day features — captures intraday demand patterns

Technical Stack

- Language: Python

- ML/DL:

lightgbm,xgboost,torch(LSTM/GRU) - Optimization:

optuna - Analysis:

pandas,numpy,scikit-learn,statsmodels - Reproducibility: GitHub Actions CI for automated notebook rendering